Aftereffects of a top DTI

Overall, mortgage brokers or any other creditors choose a maximum DTI from 43%. not, loan providers choose come across a personal debt-to-earnings proportion less than one to to demonstrate your most recent bills would not affect your capability to repay their mortgage.

As a whole, a high DTI insinuates you struggle to pay the money you owe timely, plus funds try shorter flexible for much more debt.

Simultaneously, you may not be eligible for various fund, including personal and you may lenders. Even though you do get approved loans Hot Sulphur Springs for a loan, their large financial obligation-to-earnings ratio is also yield your less beneficial terms and better notice costs as you are seen as a riskier debtor so you’re able to lenders.

Financing Certification

The greatest feeling out of a top DTI isnt becoming in a position to be eligible for money. As we now have said, a top DTI says to loan providers that you may possibly currently become lengthened too thin to look at much more personal debt. Because mortgages are usually costly than other variety of loans, lenders can refuse the job if the DTI ratio is large than simply 43%.

Naturally, other variables, such as your possessions and you may discounts, can take advantage of a role from inside the mortgage degree, so having a premier DTI does not automatically make you ineligible. Nevertheless can make it harder so you’re able to safer property loan.

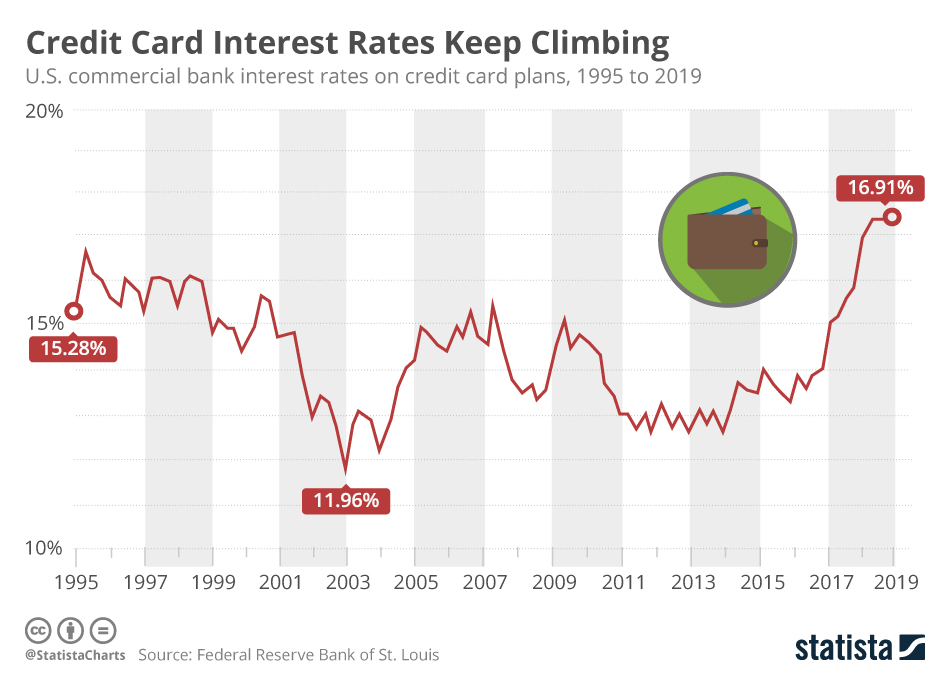

Interest rates

Even if you is safer a mortgage with a high DTI proportion, loan providers need certainly to decrease the possibility of that delivers financing. Because your large DTI ratio indicates that you might be overextending on your own currently, the lender you’ll protect themselves against their failure to repay the mortgage giving your high rates.

Large interest rates indicate spending moreover the life span of loan. Regardless of if you will be recognized for a financial loan, its imperative to determine if you want to spend significantly more due to large interest levels that impression your money of numerous many years to come.

Obtain the latest Griffin Gold application now!

Most lenders and you will mortgages need a good DTI away from 43% otherwise all the way down. Sooner, you should opt for only about 43% of disgusting month-to-month income supposed on the expense, plus another type of mortgage. Hence, for many who get a loan having a good DTI already from the 43%, you may be less inclined to score approval having a normal financing with rigorous lending conditions.

Thankfully, there are lots of mortgage programs designed for consumers which have bad credit. However, once more, the newest tough their credit while the high the DTI ratio, the higher the rates will end up being.

Your own DTI is too Highest. Now what?

For those who have a leading DTI, there are many things you can do to achieve this and you may begin reducing they before you apply for a financial loan. Several an effective way to alter your possibility of taking approved to own a home loan range from the following the:

Discover Flexible Financing

Particular money have significantly more flexible financing standards that allow you to qualify for home financing with high DTI proportion. Including, FHA loans to own very first-date home buyers ensure it is DTIs as much as 50% in some instances, even after smaller-than-finest borrowing.

Virtual assistant money certainly are the extremely versatile when it comes to lending requirements while they allow qualifying pros, productive duty service participants, and you may surviving spouses to place off only zero % towards loan.

All mortgage system and bank features different qualifying requirements, it is therefore important to see the choices to find the best financing apps predicated on your financial situation.

Re-finance The debt

You might be able to reduce your DTI proportion by the refinancing or restructuring your financial obligation. Including, you will be in a position to refinance student loans, handmade cards, signature loans, and you will existing mortgages to have less interest rate or extended payment terminology.